Members will recall from our last USS update that with the first phase of contribution increases from the 2017 valuation now in effect, the USS trustee has since the end of February been considering a proposal from Universities UK for a less costly “contingent contributions” model for USS from October. Under that proposal, an initial member contribution rate of 9.1% of salary would increase by 0.35% per year if and only if specified adverse developments materialised, while benefits would remain unchanged. This offered considerably less total funding to the Scheme than the Trustee had indicated it would like, but considerably more than the Joint Expert Panel had judged was required for prudence. UCU’s position remains that the Scheme could be adequately funded for the next three years at the pre-April contribution rates of 8% of salary from members and 18% from employers, as the JEP recommendations in combination with the March 2018 facts would support.

On Thursday of last week, USS responded to the UUK proposal. On the level of risk the Trustee is prepared to take, and therefore the price of any given level of benefits, USS remains wholly unwilling to compromise. It has restated its view that a total contribution rate of 33.7% of salaries (10.7% for members) is the correct “price” for current benefits, and that any contingent contribution arrangement must match that level of funding in the event that all contributions are triggered. The UUK proposal has accordingly been rejected.

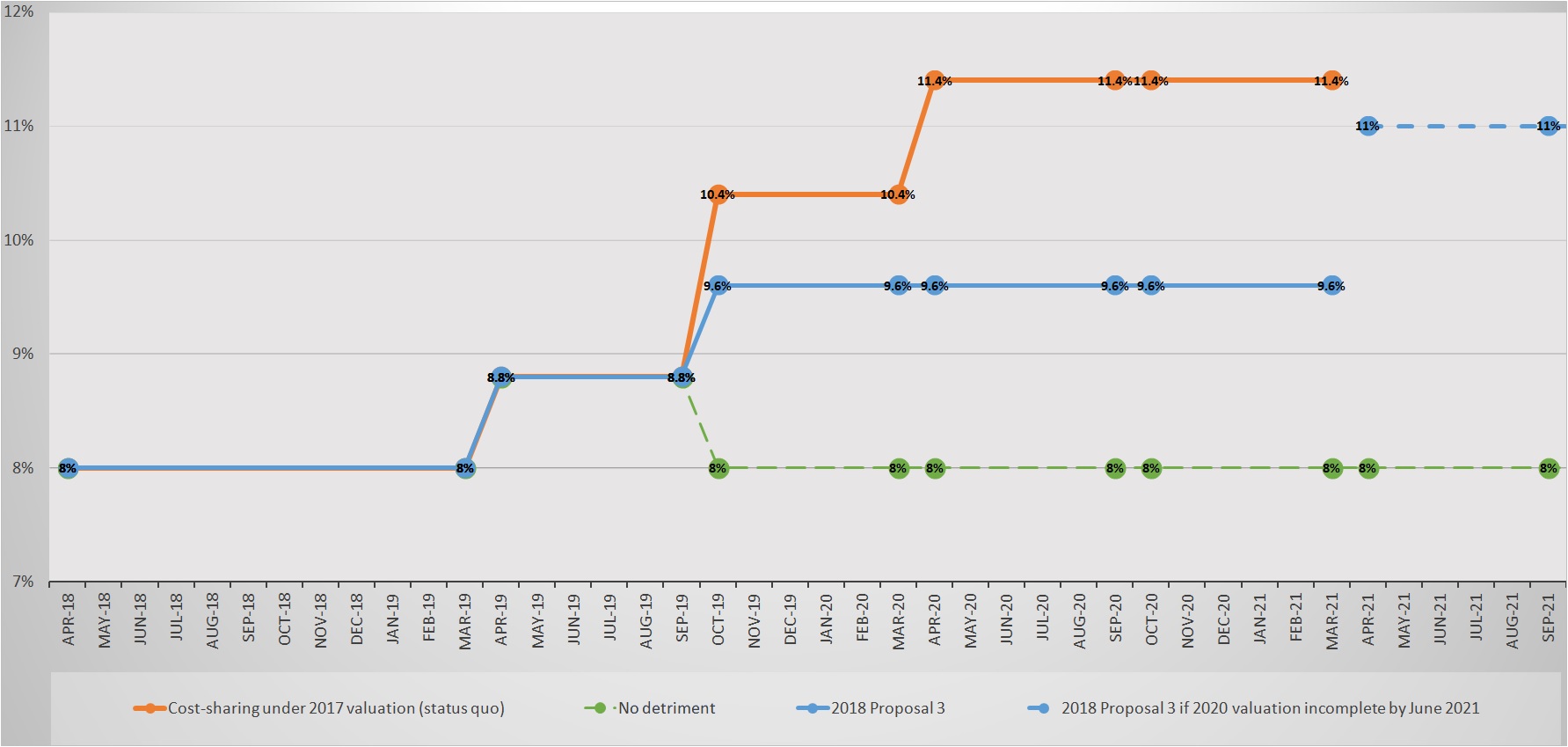

However, USS has made a new proposal, which is that a contribution level of 30.7% (9.6% for members) be adopted from October 2019 to October 2021, with a valuation as at March 2020 to provide the basis for contribution rates thereafter. If a 2020 valuation is not successfully concluded by that date, however, the contribution level would be hiked in October 2021 to 34.7% of salaries (11% for members). In effect, the proposal is for stepped contribution increases, but with the later, higher rates subject to pre-emption by a new 2020 valuation. The chart below shows the new USS proposal in solid blue, with the current cost-sharing schedule in orange. The blue dashed line from October 2021 indicates the contribution increase which would be imposed then if (and only if) no 2020 valuation is completed by the June 2021 deadline. The green dashed line at 8% represents the ideal of “no detriment”, i.e. restoration of the pre-April status quo.

Members will rightly be exasperated that the USS Trustee has refused to alter its basic approach to the valuation of the Scheme and the costing of defined benefits. Test 1 remains in place, the de-risking programme is unchanged, and Deficit Recovery Contributions remain at 5% of salaries despite the fact that 2.1% of salaries was thought sufficient in September 2017 and the deficit has reduced considerably since. (The Trustee’s rationale for this inflexibility, such as it is, can be found here.) If the new USS proposal is adopted unmodified, however, the member contribution rate of 9.6% of salaries until October 2021, with no cuts in defined benefits, compares very favourably with anything that has been on offer so far1. Employers will also be accepting a much larger share of the additional cost imposed by USS than they were previously willing to. It is inconceivable that these gains could have been made without last year’s industrial action.

Moreover, it is probable that the new USS proposal is now the only way the currently scheduled October 2019 increase to a 10.4% member contribution can be avoided, since any other way forward would either require negotiation and consultation extending beyond the statutory June valuation deadline, or involve higher contribution rates still. This means there are strong incentives for members (and employers) to accept the proposal. And yet UCU’s case against the USS valuation methodology has still been neither accepted by USS nor convincingly refuted, despite having now received powerful support from the JEP, from UUK, and from this University. The Scheme thus remains vulnerable to further degradation after October 2021, potentially including renewed pressure from employers to cut benefits in order to reduce costs.

— Sam James, Cambridge UCU President

1 Since 2017, the offers for benefits and contributions from October 2019 have been successively 20% of salary into a DC-only pot for an 8% member contribution (JNC decision, 23 January 2018); a much-reduced DB pension for an 8.7% contribution (Acas agreement, 12 March 2018); and status quo defined benefits for member contributions rising from 10.4% to 11.4% (finalised 2017 valuation, January 2019). No other proposals have been accepted by both USS and UUK, despite the recommendations of the JEP Report, which supported a total contribution rate under 30%.